Last week, I met a lawyer on my flight to Delhi. Since I had nothing better to do, I broke the ice and soon, we started discussing about my favorite topic – how do we get wealthier over the long run.

So I asked my new found lawyer friend, what does he do with his surplus funds? Immediate response – “Fixed Deposits!” So I then asked him why? And with a very perplexing look, he said – “My money grows at 6.5%. Do I need another reason?”

That is when I realized the lack of awareness that is prevalent even amongst the learned breeds of lawyers. I therefore introduced him to the concept of Debt Funds.

Debt Funds are those mutual funds which invest in debt instruments like bonds, debentures and money market instruments. But why are we comparing debt funds to fixed deposits?

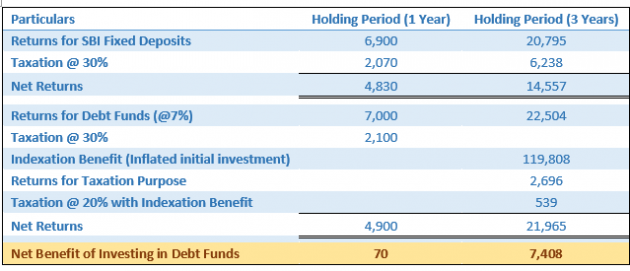

Fact 1: Debt funds on an average give an annual return of 7.0% – 8.5%. SBI 1 Year Fixed Deposit yields 6.9% interest annually, and a 3 Year Fixed Deposit yields 6.50% annually.

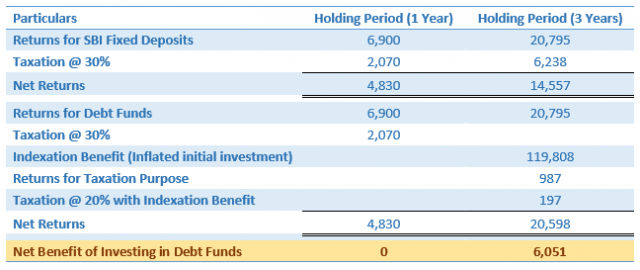

Fact 2: If money stays invested in a debt fund for more than 3 years, then you end up paying considerably lower tax on the returns from such debt funds. This is because of the indexation benefit. Indexation implies to inflating purchase cost to account for inflation. As a result, returns which are subject to taxation is reduced. Also, such reduced returns are taxed @20%. However, in case investments are held for less than 3 years, the gains are added to the income of the investor and taxed as per the income tax slab rate applicable.

Fixed deposits are taxable as per the applicable slab rate of the investor, irrespective of the holding period of investment. That doesn’t sound good at all!

Let us understand by examples:

Consider an investor with income of INR 15lacs. He is willing to invest INR 1lac. The tax slab for this investor is 30% as per the income tax slab.

Case 1: Comparison of FD vs Debt Fund, assuming different rate of returns (as per Fact 1 above)

The net gain from investing in Debt funds exceeds in both the holding periods, so the investor is better off by investing in debt funds after taxes.

Due to indexation benefit, the purchase price has been inflated from ₹100,000 to ₹119,808, thereby reducing the tax liability from ₹6,238 in FD to ₹539 in debt funds. This benefit is available when the holding period is 3 years or more.

Case 2: Let us consider a scenario where returns from debt fund are the same as that of FD

An investor is better off by ₹6,051 even if the returns are same, in case holding period exceeds 3 years. Hence, debt funds are more tax efficient than fixed deposits in every scenario.

Time you think about the funds lying in your bank account?

Read More: Will Debt Funds help your create wealth?

Great blog helped me find out whether I am earning properly on my fixed deposit account I also referred some of my friends this blog, thanks again for such a great blog.

Hi Sushant,

Thank you for the kind words. We hope that you have realized that there are other instruments and Fixed Deposit may not be the most optimal investment instrument. You can reach out to us on +91 9769356440 if you have any further queries.

We are glad that you liked our blog and have referred the same to your friends. Stay tuned for more interesting content. Please subscribe to our blog now!!

Regards,

CAGRfunds Team