Ajay, my neighbor, was a regular “fitness freak” and never failed to capture my avid respect for his assiduous dedication to his fitness regimen. Three years ago, I was impressed enough to seek his friendship and invited him over for dinner. It was across the dinner table that I discovered his personal dilemma.

His passion for physical fitness was total and amply rewarded. However, he was nursing a deep regret in that he saw no way of realizing his abiding dream of starting a fitness center. In twenty years of working as a gym instructor, he had not managed to save any money.

As a financial planning aficionado, I immediately put on my “financial adviser” hat and apprised Ajay of “Financial Fitness” – how, by following a simple set of money management skills, a stress-free life of financial well-being can be ensured.

1) Have predefined financial goals

The secret of financial stability begins with sorting and ordering priorities and with defining short term and long term goals. It is essential to achieve this clarity so that resources can be managed and plans laid out, to align with fine-tuned goals. If there is no sense of direction, the destination cannot be reached.

2) Calculate net worth

Once the goals and priorities are defined, assets and liabilities need to be assessed to determine the net worth of an individual. If a huge loan repayment is pending, an investor’s net worth may be negative, a situation that calls for urgent and concerted financial planning.

3) Manage Taxes

Taxes are often considered a necessary evil. While this may be true, there are numerous ways to harvest the benefit of government schemes and reduce taxable income, in the process. Filing tax returns before the stipulated deadlines and avoiding any direct or indirect course of tax evasion goes a long way towards inducing financial discipline.

4) Invest regularly

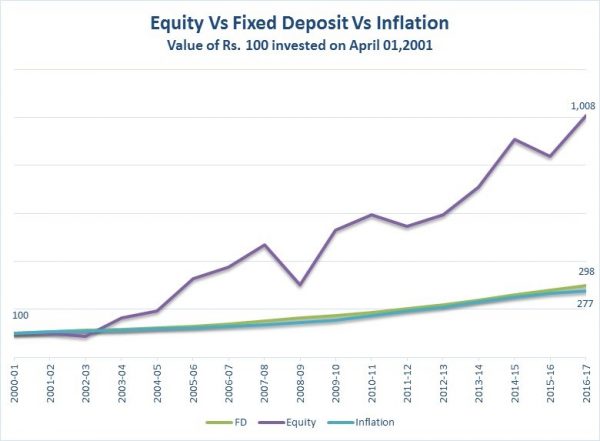

Simply depositing money in a bank cannot be the most productive way of capitalizing on savings. Investing is a wiser route to beating inflation and simultaneously building a corpus over a period of time. Align investments with pre-defined goals. It is possible that at all times sufficient funds for investments are not available; nonetheless, regular and disciplined investments should be maintained every month. Start small, but start early! Read more about this here

5) Earn as well as learn

Financial knowledge is not everyone’s forte. The lack of adequate information should not accrue as the stumbling block in financial decision making. There is no harm in consulting financial experts. Broadening the knowledge base in this domain can prove extremely rewarding. It is never too late to learn how to earn.

6) Maintain an emergency fund

If there is one thing that will remain constant, it is the ever changing scenarios that life will keep presenting as challenges. To deal with unexpected exigencies efficiently, an individual should have saved an emergency fund, which should ideally equal about 5 to 6 times of the monthly expenses. This will ensure the much needed cushion in times of emergency.