“My mother had a great deal of trouble with me, but I think she enjoyed it.” – Mark Twain

Such is motherhood – an epitome of love, dedication and care. Historically, India has been a patriarchal society – where men earn and take care of all finances and women handle an equally challenging task of running the home and taking care of the kids. Driven by her innate maternal instinct, a mother often plays a more direct role in shaping the foundation of her children’s value system and setting the direction for their beliefs and aspirations.

In the last few years, there has been a noticeable and encouraging shift in this direction – with fathers playing an increasingly important role in the upbringing of the children and women sharing the onus to earn the livelihood for the family. Times are changing, and sooner than we think!

But as mothers broaden their ambit of responsibilities, there is a remarkable scope for them to contribute to the financial planning of the family, more so to that of her children. Financial planning still remains the husband’s task and we rarely come across women approaching us to create an “education fund” for example – be it because of limited knowledge or limited interest.

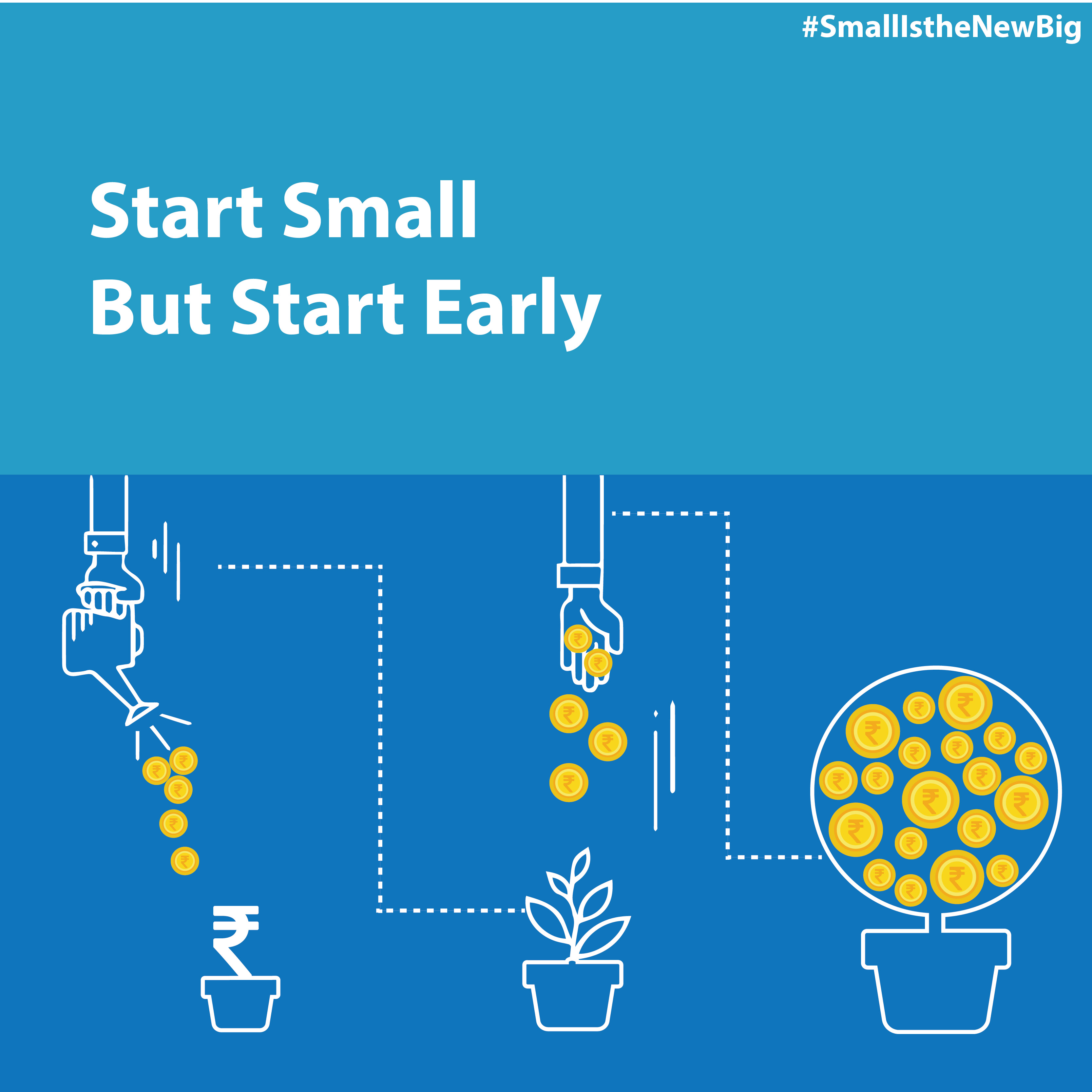

This Mother’s Day, as we celebrate motherhood, we salute all the astounding mothers out there. At the same time, we invite all mothers to take upon themselves, the responsibility to secure a bright future for their children, through diligent financial planning. While the husbands must be doing an excellent job at planning the finances of the family, this mother’s day “Gift an SIP” to your child – an expression of love, manifested uniquely and responsibly!