CAGR Insights is a weekly newsletter full of insights from around the world of the web.

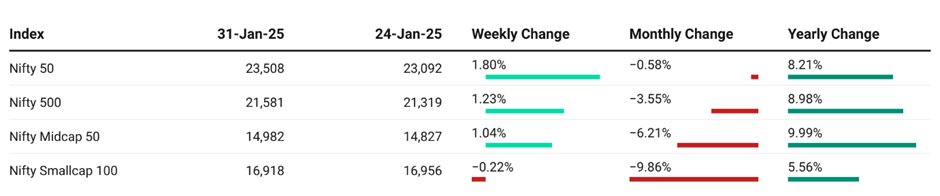

Chart Ki Baat

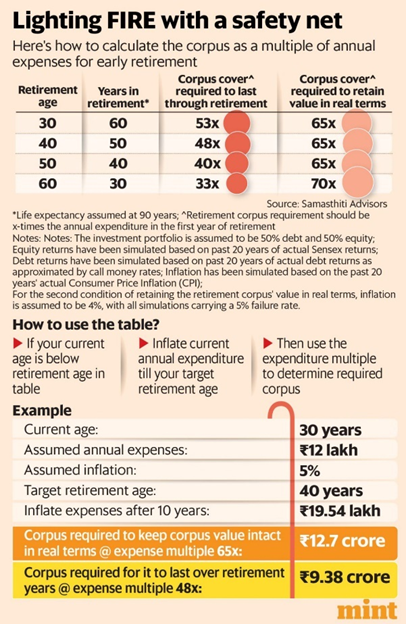

Gyaan Ki Baat

The Reserve Bank of India (RBI) Monetary Policy Committee (MPC) concluded its meeting on February 7, 2025, announcing key decisions impacting the Indian economy12. This was the first MPC meet chaired by the newly appointed Governor Sanjay Malhotra12.

Key Decisions and Announcements:

- Repo Rate Cut: The MPC voted to cut the repo rate by 25 basis points, bringing it down to 6.25%. This is the first rate cut in nearly five years, with the last cut occurring in May 2020134. The repo rate had remained unchanged at 6.5% since February 20234.

- Unanimous Vote: The MPC voted unanimously to maintain a ‘neutral’ policy stance4.

- GDP Growth Projection: For the financial year 2024-25, the RBI has projected India’s real GDP growth at 7.2%3.

- Inflation Target: The MPC aims to continue improving macro-outcomes in the best interest of the economy and will use flexible inflation targeting to make the best macro decisions. The average inflation has been lower since flexible inflation targeting was adopted, and CPI has mostly stayed aligned with the target4. The RBI is aiming for a fiscal deficit of 4.8% of GDP for the current year and is targeting 4.4% in 2025-263.

- Liquidity Boost: The RBI had previously infused approximately ₹1.50 trillion into the banking system through open market bond purchases, FX swaps, and a 56-day variable rate repo.

Personal Finance

- Old vs New Tax Regime: Which Is Better New or Old Tax Regime for Salaried Employees? The 2025 budget introduces new tax slabs with lower rates, enhanced rebates, and deductions under the new regime, aiming to simplify tax filing and reduce liabilities. Want to know which tax regime benefits you the most? Read on to make the smartest tax choice for your future! Read here

- RBI revises credit reporting rule: How it’s going to affect your credit score: RBI’s new 15-day credit reporting rule, effective from January 2025, ensures faster, more accurate credit scores. Borrowers will benefit from quicker updates on repayments, leading to better loan approvals and interest rates. Read here

- Big relief for home loan borrowers as EMIs to fall by 1.8% on a 20 year loan tenure as RBI reduced repo rate by 25 bps: In a major relief for home loan borrowers, RBI cuts the repo rate by 25 basis points after 5 years, expected to lower home loan interest rates. This move aims to support GDP growth and boost economic activity by reducing borrowing costs. Find out how this impacts your home loan rates! Read here

Investing

- Category I and II AIFs get tax clarity in the Budget FY26: The government has clarified that income from Category I and II AIFs will be treated as capital gains, taxed at 12.5%, instead of business income taxed at up to 39%. This move, effective April 2026, aims to boost investor confidence and provide tax relief. To know more about the changes. Read here

- End of Sovereign Gold Bonds – Alternatives to SGB Now (2025)? The government’s decision to phase out Sovereign Gold Bonds (SGBs) leaves investors looking for new gold investment opportunities. Gold ETFs, Mutual Funds, and physical gold are gaining attention. Want to know the best alternatives for your portfolio? Read here

- 5 Common Investing Mistakes That Destroy Your Returns: Successful investing requires starting early to harness compounding, resisting the urge to time the market, and managing emotional reactions like fear and greed. Align your risk tolerance with life stages and prioritize understanding your investments for long-term wealth creation. Discover the 5 key mistakes that could derail your investment journey. Watch here

Economy & Sectors

- Can a consumption boost save India’s slowing economy? India’s 2025 budget targets middle-class consumption with tax cuts, aiming to boost the economy. Despite a 1-trillion-rupee revenue shortfall, experts stress the need for broader reforms, like capital expenditure and job creation, to sustain growth amid challenges. Find out what’s next for India’s economy. Read here

- India’s insurance landscape: Poised for growth: The rapid growth in the insurance sector can be attributed to the increased participation of private players, use of technology, product innovation, improvement in distribution capabilities and improvement in operational efficiencies. Read here

- India budget opts for economic sugar rush over reform: India’s 2025 budget, the first under PM Modi’s third term, focused on short-term relief with middle-class tax cuts but lacked long-term growth reforms. Despite forecasts of slower GDP growth (6.4%), experts argue more comprehensive agricultural, labor, and market reforms are needed for sustained growth. Find out how this budget impacts India’s economic future.Read here

Check out CAGRwealth smallcase portfolios

Our smallcase portfolios are ranking well in the smallcase universe in terms of 1-year returns.

• CFF (launched in June 2022) – Ranked 1st amongst smallcase with medium volatility.

• CVM (launched in May 2022) – Ranked among Top 20 across the Momentum smallcase universe.

Do check it out here

****

That’s it from our side. Have a great weekend ahead!

If you have any feedback that you would like to share, simply reply to this email.

The content of this newsletter is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction. The content is distributed for informational purposes only and should not be construed as investment advice or a recommendation to sell or buy any security or other investment or undertake any investment strategy. There are no warranties, expressed or implied, as to the accuracy, completeness, or results obtained from any information outlined in this newsletter unless mentioned explicitly. The writer may have positions in and may, from time to time, make purchases or sales of the securities or other investments discussed or evaluated in this newsletter.