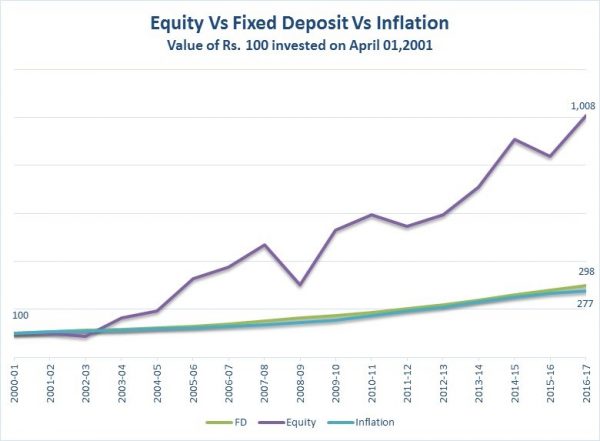

If you were standing at the crossroads, in a new city, unsure of which direction to take and you observe 9 out of 10 people moving towards the left, isn’t it likely you will follow the more numerous group? This is an illustration of the herd mentality that we are all prone to, especially in unfamiliar situations. “When in doubt, play safe”, is the philosophy that drives this behavior. Ever wondered why this happens?

1) Social Acceptance

It is natural for us to crave acceptance in a group and wish not to be perceived as someone who goes against the crowd. This social pressure often compels us to choose options we would otherwise not have considered.

2) The Ad Populum Fallacy

We are ensnared by this fallacy when we happen to be unclear about the choices to opt for. Believing that we lack some information that others have access to, we choose to endorse the choices of those others, even if the preference may appear irrational at first. We convince ourselves that it is unlikely that so many people can be wrong simultaneously.

If many believe in a particular outcome, the chances of them being correct are high, isn’t it?

This may or may not be true. ‘Argumentum ad Verecundiam’ or ‘Argument from Authority’ is also sometimes termed ‘Appeal to False Authority’ or ‘Appeal to Unqualified Authority’. Argument from authority illustrates a statement that is authenticated by expert opinion. The latter two terms refer to positions that are adopted on the basis of hearsay. We often encounter hearsay in stock markets. Millions of people trade in equity stocks based on “tips” they receive from friends or relatives and many end up burning their fingers.

The inclination of investors, to follow the herd instinct is rooted in the quest for the latest trends in the financial markets. Which mutual fund scheme is fetching the greatest returns or which scheme is a part of some top investor’s portfolio? Did equity outperform bonds in the financial year or not? Based on the answers to such questions, investors switch back and forth rapidly, without realizing that the cost involved in such a process is going to eat into their profits, if at all they make any.

How do we avoid such behavior?

Should investors stop looking at trends and suggestions? It will be wrong to eliminate networking altogether. Research and meticulously acquired expertise are the two pillars, which serve to neutralize the risk of following the crowd.

This adverse impact of herd behavior is most visibly apparent in the realm of financial markets. An investor needs to overcome the fear of isolation and drive innovative investment strategy. Towards this end, he must either gain the expertise to manage his investments with acumen or take the help of a reliable advisor, who can guide him.