Tax Saving Mutual Funds or ELSS (Equity Linked Savings Scheme) funds are a type of mutual funds which give you tax benefits under section 80C and also enable growth in your investment. Like all other equity mutual funds, they too invest in the equity market. So what makes them unique and desirable?

- Potential of generating high returns (historically, the good funds have generated an average annual return of more than 15% )

- Least lock-in period of 3 years compared to other tax-saving options

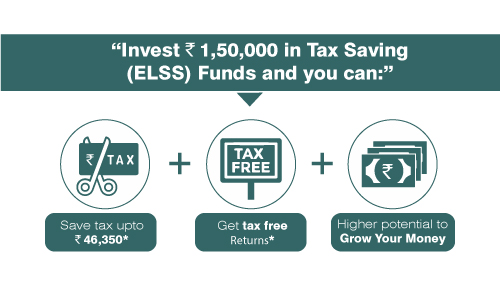

- Deduction of ₹1.5 Lacs every year from taxable income, thus a saving of up to INR 45000 in tax

- More equity exposure (linked with higher returns) than any other tax saving options

- Available to HUFs also (Unlike individuals, HUFs have limited alternatives to save tax)

So, basically an individual or HUF (Hindu Undivided Family) can avail an exemption of ₹1.5 Lacs from their total taxable income in every financial year by investing in ELSS Mutual Funds under Sec 80C of Income Tax Act, 1961. In addition to this, a capital gain of ₹1 Lac is tax-free. Gains above ₹1 Lac are taxable @10% under Growth plans. Dividend plans will have a 10% tax levied from April, 2018.

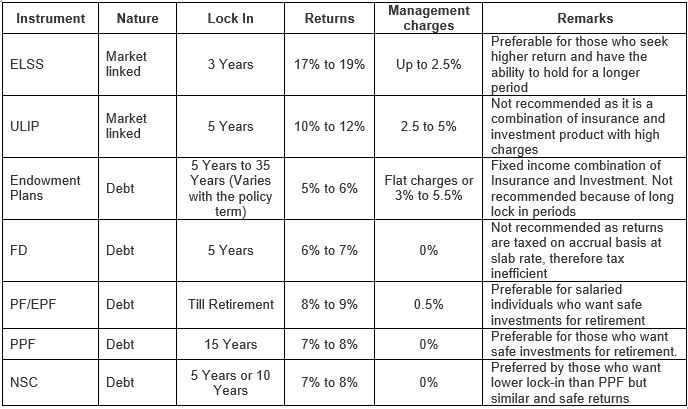

How is ELSS better than other investment options (ULIP, FD, NPS, PPF, and NSC)?

ELSS will therefore be appealing to an investor who has a higher risk appetite as ELSS funds have the potential to outperform and generate better returns than FDs, NSCs, and PPF/EPF.

ELSS will therefore be appealing to an investor who has a higher risk appetite as ELSS funds have the potential to outperform and generate better returns than FDs, NSCs, and PPF/EPF.

Final Thoughts:

There’s a widespread misconception that equity is too risky for older investors or for retirees and therefore they should not use ELSS. The truth being that every investor, who has a high risk appetite and wishes to invest in equity, has ELSS as a great investment option. It benefits your finances by saving on tax and generating better returns than traditional investment options.

The main issue that we, as Indians, face is inflation (6-7%). Fixed deposits and similar investments take a big hit because of inflation and the falling rupee rate. The returns are simply not rewarding and barely help to keep the value of the principal investment. For an investor saving for his children’s education, FD may not suffice as education inflation grows by 15% while for a retired person, prices for goods and services from healthcare grow by 20% due to inflation. Such long term investments maybe very underwhelming.

Of course, like all equity investments, the best way of investing in ELSS funds is through monthly SIPs throughout the year. Equity investment is a higher risk instrument over the short term. However over a span over 3 to 5 years, the market fluctuations are averaged out and the returns are usually healthy.

Investors can choose to invest lump sum too. Although, it is riskier than SIP as your returns can vary with the market highs and low. During a market high, it seems attractive to invest and during lows investors rush to stop investments. This is where they make lose on an opportunity. High markets fetch lower units and hence lower returns. Low markets fetch higher units and hence higher returns. Although, timing the market is never certain and it’s advisable to invest through SIPs as market highs and lows will produce a healthy average return in the long run.