India loves nothing more than its cricket. And cricket is best epitomized in the all exciting and our very own Indian Premier League. However, if we spare a thought, IPL is not just a game. The learnings that we can derive from IPL are applicable in multiple facets of life.

Let us see how you can takeaway 5 things that will help us manage your money better.

1. Balance your portfolio

T20 as a sport demonstrates how a team cannot harness dependency on a single player. A winning team is a combination of the right mix of bowlers, batsmen and all-rounders.

Likewise, a portfolio which is diversified across various asset classes is always preferable over one which focuses on a single asset class. Imagine you invest all your savings in that house you had always dreamt of. While you now own the place you stay in, you don’t know how to fund the medical emergency that has suddenly cropped up in the family. Hence, it is essential that you map your investments to various goals and create a balanced portfolio.

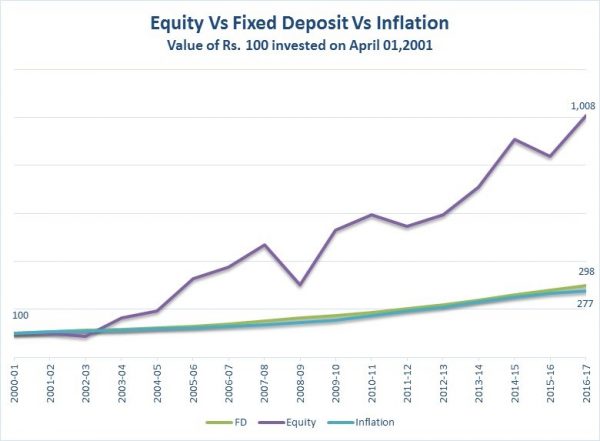

2. Start planning early

IPL teams start wracking their brains right from the day they have to pick their players: which players should be retained, what would be the best combination in the given budget, is the value of a player worth his cost?

Similarly, an early planning for investing is always worthwhile. Not only does it give us better control over our finances but also gives us substantial time to plan for our goals. It is therefore important to understand every step in financial planning before you actually start investing.

3. What’s hyped isn’t always the best

IPL-1 is a great reflection of the famous catchphrase ‘all that glitters is not gold’. With their multi-million dollar wallets, pundits betted on teams like Mumbai Indians and Delhi Daredevils. The season, however, ended with the shoestring-budgeted Rajasthan Royals taking the trophy home. People thought that a bigger budget meant winning the trophy. But if only it was that simple!

Hype can often be misleading. We often tend to fall prey to herd mentality. However, it is of utmost criticality that you decipher facts yourself and look at all the important statistics with the help of an expert.

4. Keep your calm: Don’t quit on a winning strategy

IPL-2015 – a case in point. Mumbai Indians lost the first four matches of the season and were at the bottom of the table. But they knew they had a winning mix. They chose to stick to their guns and treaded with caution and patience. Result – They brought the trophy back home.

So, if you know that you have a winning portfolio or a winning strategy, don’t quit! Don’t be bogged down by short term fluctuations and focus on the long term.

5. Some advice along the way always pays off

We have often seen the cricketing maestros contributing their bit in mentoring and guiding the players off the field.

Financial planning which is a highly knowledge driven domain, is better done when planned along with a financial advisor. While your current knowledge may seem to be sufficient and adequate, you might not be as aware of the latest developments or specific implications of different instruments and investment avenues. It therefore always pays off to consult an advisor before you take that big leap with your hard earned money.